Compare our best 0% money transfer credit cards

Transfer cash to your bank account with a credit card

Check eligibility and compare 0% money transfer credit cards

What is a money transfer card?

A money transfer card allows you to borrow money from your credit card and transfer it directly into your bank account. Typically, there is a fee for this service, usually around 4% of the amount transferred.

How does it work?

The transfer takes place after you ask your provider to transfer the money into an account of your choosing.

This should not be confused with withdrawing money from your credit card from an ATM, which is known as a "cash advance" and typically results in extra fees and interest charges.

The money transfer facility is useful if you need to pay off an overdraft, or if you need cash to pay for goods and services. An example would be paying a builder or plumber because they don't accept credit card payments.

With a 0% money transfer credit card, not only can you move cash into your bank account, but you can pay off your balance without paying interest for a set period. This could be up to a year or more.

However, to qualify for the longest 0% interest periods, you need to have a good credit score. A cash transfer fee, typically of 3% to 5% would still normally apply.

Why would you get a money transfer card?

Money transfer credit cards are good at doing a very specific set of things.

But if you step outside their specialist areas, they become at best a compromise and quite possibly the entirely wrong product to take out.

So, what are they good for?

The first thing they can help with is clearing an overdraft. With banks now charging as much as 40% interest on overdrafts, paying off that debt with a 0% credit card could save you a lot of money.

The second thing they are highly effective at is providing a cheap loan that you can use to pay friends, tradespeople or anyone else you owe money to but who doesn't take credit cards.

But if you're looking to save on existing credit card debt, you'll almost certainly get a better deal with a balance transfer credit card than with a money transfer card.

And if you're looking to spend the money you transfer on anything you can buy directly with a credit card, a 0% purchase card will work out cheaper.

If you're looking to borrow more than £5,000, it's worth looking into a traditional loan as well, then comparing the total costs of each.

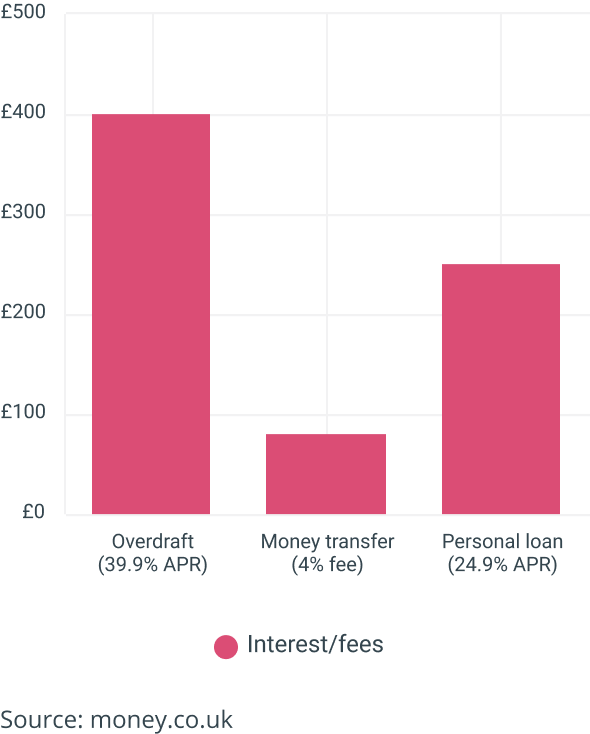

Borrowing £2,000 over 12 months with a loan, money transfer or overdraft

Pros and cons

Pros

Cons

How to choose the best money transfer card

When comparing money transfer cards there are a few key factors you should consider before picking the one you want:

Interest free period

This is the period during which you don’t pay interest on your balance, and begins once you’ve made the transfer. In most cases this should happen within days of receiving the card. The longer the interest free period, the less you’ll have to pay each month to pay off your debt before the 0% period ends.

Money transfer fee

Most money transfer credit cards will charge a fee to transfer the money. This is either a flat fee or a small percentage of the amount you want to transfer - usually around 3% to 5% of the amount you transfer - and is added to the balance on your new card.

Interest rate

This is the rate you’ll be charged to borrow on your credit card after the interest free period ends. It’s often known as the revert rate. If you plan on continuing to use your card after the 0% period ends, it’s important to get a card with the lowest rate you’ll be accepted for, especially if you think you’ll be carrying over a balance on a regular basis.

Check eligibility and compare 0% money transfer credit cards

What if I can't afford to keep up with payments?

If you’re having trouble keeping up with your payments, don’t be afraid to ask for help. There are several independent services you can contact for free advice.

As well as helping you to manage your debts, these services can also ensure you are receiving all the benefits you are entitled to, including tax credits. This could help top up your income and go towards paying off your debts.

StepChange - StepChange is a charity providing advice and help on budget and debt management. It has a helpline that provides free and independent advice.

Citizens Advice - You can find your local Citizens Advice in the phone book or through its website. Citizens Advice can advise you on legal and financial issues.

National Debtline - The National Debtline offers confidential, free advice to people facing debt problems in England, Wales and Scotland.

“If you're struggling with debt, you have a right to 60 days 'breathing space' where creditors aren't allowed to contact you and interest and charges are frozen. But you need to speak to a debt adviser to claim it.”

Jargon buster

FAQs

In depth guides to credit cards

About the author

Didn’t find what you were looking for?

Below you can find a list of our most popular credit cards:

Customer Reviews

Everything you need to gain credit for…

Very fast and efficient. From start to finish it was easy to follow the application.

Great website

We’ve been featured in