Moving house is expensive, especially if you need to buy a lot of furniture to fill it, you need to equip a kitchen or you have some home improvements to pay for. A 0% purchase card can let you spread the cost of these purchases interest-free.

- >

- Credit cards>

- Purchases credit cards

Compare our best 0% purchase credit cards

Spread the cost of your spending interest free with a 0% purchase credit card

Spread the cost of spending

Compare top 0% interest offers and check your eligibility in minutes without affecting your credit score.

Check eligibility and compare 0% purchase credit cards

We've partnered with Experian to help you find cards that match your needs — without affecting your credit score

1

Tell us a little about your finances and card preferences

2

See your personalised card matches with approval chances

3

Compare features and apply for the card you like best

money.co.uk is a credit broker, not a lender, for consumer credit. Our services are provided at no cost to you. We may receive a commission from the companies we refer you to, but this does not affect what you will pay for the product you choose.

What is a 0% purchase card?

A 0% purchase credit card lets you spread the cost of your spending over several months without paying any interest.

For example, if you use a 0% purchase card with a 24-month interest-free period to buy something for £1,500, you could pay it off in equal instalments of £62.50 per month, without any added interest.

Interest-free periods can vary, typically lasting anywhere from three to 26 months. The exact length you’re offered will depend on your credit history and financial situation.

Once the 0% period ends, any remaining balance will start accruing interest at the card’s standard rate, so it’s always best to clear your debt before then to avoid extra costs.

Why get a 0% purchase credit card?

![If you're moving house]()

If you're moving house

Moving house is expensive, especially if you need to buy a lot of furniture to fill it, you need to equip a kitchen or you have some home improvements to pay for. A 0% purchase card can let you spread the cost of these purchases interest-free.

![If you're planning a big holiday]()

If you're planning a big holiday

Getting a 0% purchase card ahead of a big trip abroad can let you pay for flights and accommodation, then pay back the money in instalments over the introductory period. You also get extra refund rights if your holiday is cancelled thanks to Section 75 of the Consumer Credit Act.

![If you're getting married]()

If you're getting married

Weddings are one of the most expensive days of your life but are planned months in advance. Interest-free purchase cards come into their own when you know you'll be spending a lot of cash in a short amount of time and want to split that cost over months. In many ways, it's a perfect match.

![If you're having a baby]()

If you're having a baby

Preparing for a new arrival can be expensive. You can use a 0% purchase card to cover the upfront costs of essentials like car seats, cots, and prams, then pay the total back in manageable, interest-free instalments.

Why get a 0% purchase credit card?

If you're moving house

If you're planning a big holiday

Getting a 0% purchase card ahead of a big trip abroad can let you pay for flights and accommodation, then pay back the money in instalments over the introductory period. You also get extra refund rights if your holiday is cancelled thanks to Section 75 of the Consumer Credit Act.

If you're getting married

Weddings are one of the most expensive days of your life but are planned months in advance. Interest-free purchase cards come into their own when you know you'll be spending a lot of cash in a short amount of time and want to split that cost over months. In many ways, it's a perfect match.

If you're having a baby

Preparing for a new arrival can be expensive. You can use a 0% purchase card to cover the upfront costs of essentials like car seats, cots, and prams, then pay the total back in manageable, interest-free instalments.

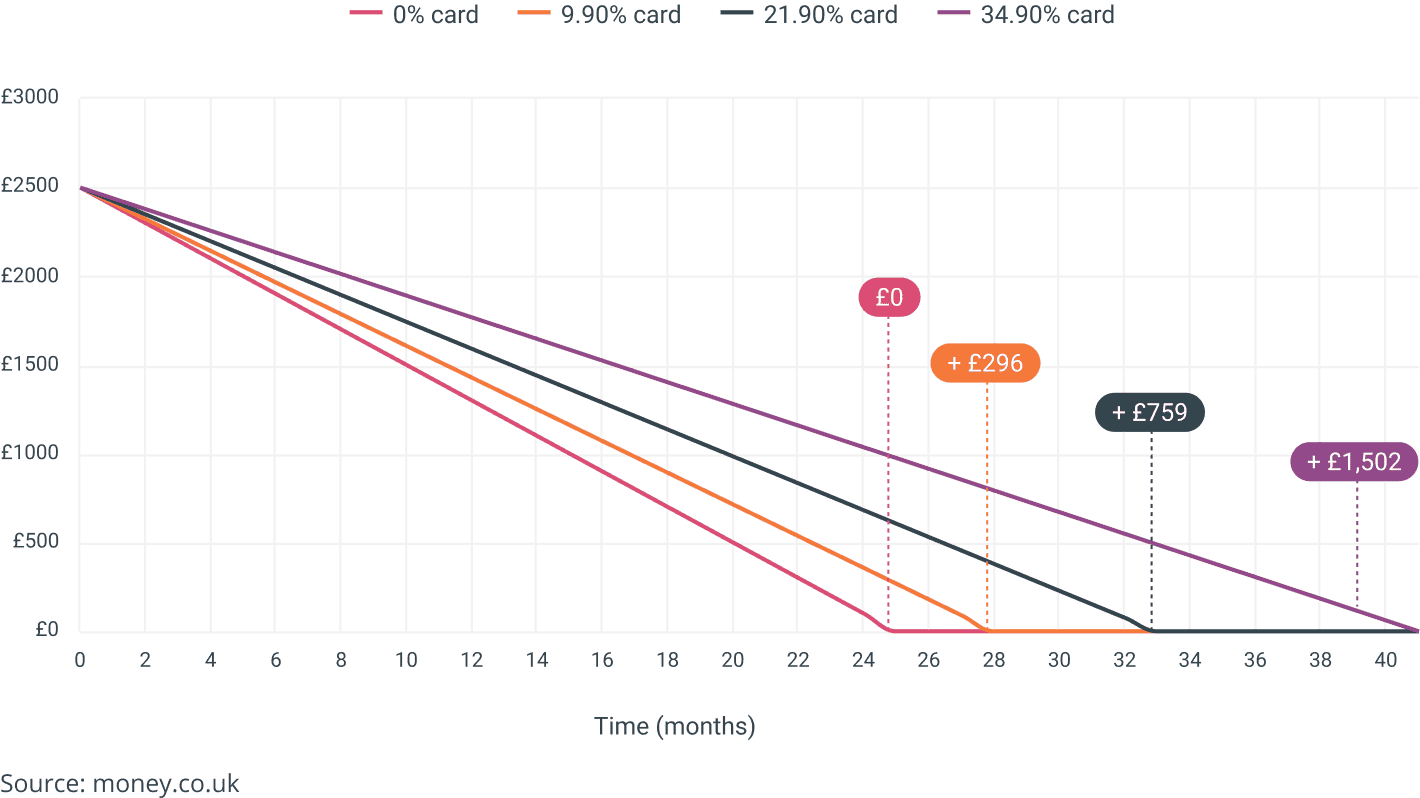

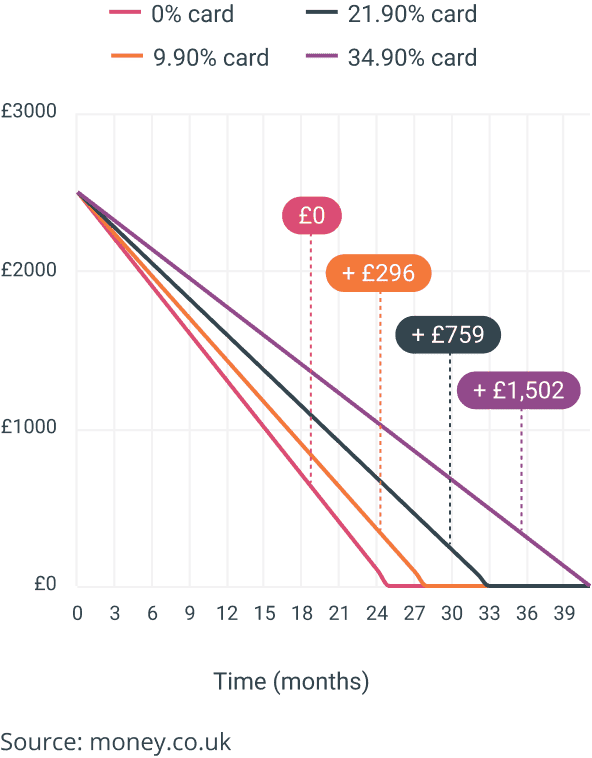

How much interest can you save with a 0% purchase card?

How an interest-free purchase card changes what you pay back and how fast you clear a balance of £2,500, assuming a fixed monthly payment of £100.

How to choose a 0% purchase credit card

When trying to pick the best 0% purchase card, there are four main features you need to consider.

Assess the length of the 0% offer

The first thing to look for is the 0% interest period during which you don’t pay any interest on your balance. Ideally, you’ll want to choose the longest 0% interest period you can be accepted for. That way, you can pay off your balance over a more extended period and keep your monthly payments as low as possible.

Consider the revert rate (APR)

This is the interest rate you’ll be charged once the 0% interest period ends. If you plan to continue using the card after the 0% deal ends, you’ll want the revert rate to be as low as you can get. This is especially true if you’re likely to have a revolving balance on the card (a balance you carry over from one month to the next).

Watch out for transaction fees

Credit cards typically charge fees for certain kinds of transactions. For example, foreign transaction fees for using the card abroad and cash advance fees for using your card to withdraw cash from an ATM. If you’re unlikely to use your card for any of these transactions, these fees shouldn’t matter. But if you are, make sure you look for a card with low or zero fees.

Check for extra perks

While the interest-free period is the main attraction, some cards offer additional benefits like cashback on your spending, reward points, or discounts with specific retailers. If you are torn between two cards with similar 0% offers, these extras could be the deciding factor.

What sort of interest free purchase cards are available

![0% purchase and balance transfer cards]()

0% purchase and balance transfer cards

These "all-rounder" cards offer an interest-free period on both new spending and existing debt you transfer from other cards. They can be very convenient for managing all your finances in one place, but use caution: the 0% periods for purchases and balance transfers often differ in length, and the balance transfer portion usually comes with a fee.

![Rewards 0% purchase cards]()

Rewards 0% purchase cards

Some cards let you double up on benefits: spreading the cost of your purchases interest-free while earning perks on that spending. These extras can range from supermarket loyalty points and air miles (e.g. Avios and Virgin Points) to direct cashback paid into your account.

![Bad credit 0% purchase cards]()

Bad credit 0% purchase cards

If your credit score isn’t perfect, you may still have options. These cards generally offer shorter interest-free periods — typically between three and six months — and lower credit limits than standard cards. However, they can still be a valuable tool for spreading costs while you work on improving your credit rating.

What sort of interest free purchase cards are available

0% purchase and balance transfer cards

These "all-rounder" cards offer an interest-free period on both new spending and existing debt you transfer from other cards. They can be very convenient for managing all your finances in one place, but use caution: the 0% periods for purchases and balance transfers often differ in length, and the balance transfer portion usually comes with a fee.

Rewards 0% purchase cards

Some cards let you double up on benefits: spreading the cost of your purchases interest-free while earning perks on that spending. These extras can range from supermarket loyalty points and air miles (e.g. Avios and Virgin Points) to direct cashback paid into your account.

Bad credit 0% purchase cards

If your credit score isn’t perfect, you may still have options. These cards generally offer shorter interest-free periods — typically between three and six months — and lower credit limits than standard cards. However, they can still be a valuable tool for spreading costs while you work on improving your credit rating.

The 3 golden rules of 0% purchase cards

To get the most out of your card without getting stung by hidden costs, stick to these three principles:

Never miss a monthly payment

One of the conditions of having a credit card is you must make monthly repayments of at least a minimum sum. But, as only paying the minimum amount each month would leave you still owing money when your 0% term ends, aim to repay more each month.

Clear your balance before the 0% deal ends

Mark the 0% end date in your calendar. If you still have a balance after this date, the interest rate will shoot up to the standard APR. To avoid this, divide your total spend by the number of interest-free months and set your monthly payments to cover that amount.

Don’t use the card for cash withdrawals

The 0% offer almost always applies to purchases only. If you use your credit card to withdraw cash from an ATM or buy travel money, you will usually be charged a fee and high interest from the moment you take the money out.

How much can I borrow with a 0% purchase card?

The amount you can borrow depends on your credit limit. This is the maximum amount your provider is willing to let you borrow on your credit card, and it will depend on factors such as your credit history, your income and how much debt you already have.

The credit limit of a credit card can range from just a few hundred pounds to tens of thousands of pounds. You can borrow any amount at any time within this limit.

Most credit card providers won’t tell you your credit limit until after you’ve applied for your card and they’ve assessed your suitability for the card you’ve chosen.

Why use our eligibility checker?

Applying for a credit card and getting rejected can leave a mark on your credit report. Our eligibility checker removes the guesswork. It matches you with the cards you are most likely to get based on your needs and financial circumstances, helping you apply with confidence and protecting your credit rating.

Check eligibility and compare 0% purchase credit cards

We've partnered with Experian to help you find cards that match your needs — without affecting your credit score

1

Tell us a little about your finances and card preferences

2

See your personalised card matches with approval chances

3

Compare features and apply for the card you like best

What to think about before applying for a 0% purchase card

Will it arrive in time?

If you're trying to snap up a great deal on a new bike, for example, you need to ask yourself if your card will arrive before the offer on the bicycle expires. Most credit cards arrive within 10 working days after your application is accepted, so if that’s too late, you could end up paying more. 0% purchase cards work best when you know in advance that you'll be spending big and can plan for it.

Make a plan to pay it off

0% purchase cards are not free money. In fact, if you don't clear your balance before the introductory 0% period ends, they can become quite expensive as interest will be charged on your remaining balance. Make sure you know how you'll be paying the card off and how long you have to do it before you start spending.

Find your limits

Once you know your credit limit, make absolutely sure you don't go over it. Missing a payment or breaching your credit limit could mean you fall foul of the card's terms and conditions, and you could lose your 0% period on your entire balance.

What are the alternatives to a 0% purchase card?

Before deciding if a 0% purchase card is right for you, it's worth comparing it against other borrowing options to see which fits your needs best.

Personal loan

Best for: Large expenses (e.g., a new car or home renovation) or those who prefer fixed monthly payments.

How it works: If you need to borrow a larger sum — often up to £50,000 — a personal loan is usually more suitable than a credit card, which has lower limits. You receive a lump sum and pay it back over a fixed term (typically 1 to 7 years).

The trade-off: Unlike a 0% card, you will usually pay interest. However, rates are often much lower than standard credit card APRs, especially for borrowing between £7,500 and £25,000.

Overdraft

Best for: Short-term, small borrowing or emergency cash flow.

How it works: An overdraft lets you dip into negative territory in your current account. It is quick to arrange and often instantly available.

The trade-off: Interest rates on overdrafts can be very high (often higher than credit cards). It is best suited for dipping in and out of for a few days, rather than carrying a debt for months. Try to find an account with an interest-free buffer if possible.

Money transfer credit card

Best for: Paying for services where credit cards aren’t accepted (e.g., a plumber or builder).

How it works: This specialised card allows you to transfer cash from the card directly into your bank account. You can then spend that cash as you please. Like purchase cards, many offer 0% interest periods.

The trade-off: There is almost always a transfer fee (typically 3% to 5%) to move the money. Also, you must clear the balance before the 0% period ends to avoid high interest charges.

Watch our video on how 0% purchase credit cards work

Can you get a 0% purchase card with bad credit?

A less-than-perfect credit rating doesn't mean you'll automatically be rejected for cards - but it can limit your choices.

Each provider makes up its own mind about what it considers important when looking at an application. That means even if you've been rejected by one credit card provider, you might not be rejected by another. But a rejection letter or email from one card provider should absolutely not be seen as a signal to apply to everybody else.

Card lenders share details of who's applying for what with credit reference agencies – lots of applications in a short space of time can make you look desperate for cash and that will actively hurt your chances of being accepted.

The key is to use an eligibility checker before applying to see what you're more likely to be approved for. People with better credit scores will generally qualify for more cards, with longer 0% purchase periods.

You will see the number of deals and the length of the interest-free periods go down the worse your credit score gets. But even with a bad credit rating, you might still find someone willing to offer you a deal.

Interest free purchases card jargon buster

APR

APR stands for “Annual Percentage Rate” and is the total cost of borrowing over 12 months. If you pay your balance in full and on time, you will not pay interest.

Annual fee

The fixed cost associated with maintaining certain credit card accounts. It appears as a single lump sum on your statement once a year. This is a standard account charge and is separate from interest payments or transaction fees.

Cash withdrawal

Withdrawing funds from an ATM using your credit card attracts a specific fee (unless you have a travel credit card that doesn't impose cash withdrawal fees at ATMs) and daily interest charged from the moment you take the money out. Be aware that providers often apply these same expensive rules to "cash-like" transactions — such as buying foreign currency, stocks, or placing bets — categorising them exactly the same as an ATM withdrawal.

Credit limit

Your credit limit is the amount you can borrow on your credit card at any one time. If you exceed this amount, you can be charged a fee — typically £12 — and it can leave a mark on your credit report. You won’t usually find out your credit limit until the end of an application process, although you can ask your provider to increase — or decrease — your credit limit at any time.

Credit limits are set based on your credit history and your earnings. Once you've reached your credit limit, you need to make a payment to bring down your balance before you can use the card again. Find out more in our guide to credit limits.

Credit score

Your credit score is calculated based on your credit history. Each credit reference agency has its own method of calculating this. Your credit score will go up for things like making payments on time and down for things like being late or defaulting on a loan. Typically, the higher your score, the more likely you are to be offered a lower rate of interest or higher credit limit.

There is no absolute pass or fail mark attached to a credit score, with each lender making its own decision on what it considers acceptable.

Direct Debit

An automated payment method where you authorise a company to collect money from your bank account. It is the most common way to pay credit card bills because it ensures you never miss a due date. You can set it up to collect the minimum payment, a fixed amount, or the full balance every month.

Eligibility criteria

The minimum standards you need to satisfy before a provider will consider your application. This typically involves your age, employment status, and salary. You should check these carefully before applying to avoid unnecessary rejections, though meeting them does not automatically guarantee you will get the card.

Foreign transaction fees

The extra cost added to purchases made in a foreign currency. Standard credit cards typically add a fee of around 2.75% to 2.99% to the exchange rate set by Visa, Mastercard, or Amex. Some specialist travel credit cards waive these fees, though you should still avoid withdrawing cash as this usually attracts interest immediately.

Interest-free credit

Interest-free credit cards allow you to either transfer a balance, make purchases or transfer cash to a current account without paying any interest on your balance for a set period. However, you must keep making at least the minimum monthly repayment during this time.

Once the 0% deal is over, you will be charged interest on any remaining debt at your standard APR. With balance transfers and money transfers, you will usually have to pay a transfer fee.

Introductory offer

Credit card introductory offers include bonus reward points, extra cashback, 0% on balance transfers or 0% on purchases.

Introductory offers are used to attract new customers, but once they expire, they revert to the standard offer or rate. When this happens, you should check if you’re still getting the best deal or whether you need to switch to a different credit card.

The pros and cons of purchase credit cards

Pros

Interest-free borrowing: This is the headline benefit. You can borrow money to make large purchases and pay it back over time without paying a penny in interest, which is usually cheaper than a personal loan or overdraft.

Purchase protection: When you buy something costing more than £100 and up to £30,000 using a credit card, you are covered by Section 75 of the Consumer Credit Act. This means if the retailer goes bust or the item is faulty or not delivered, the card provider can refund you.

Build your credit score: If you make your payments on time and stay within your limit, using a credit card responsibly is one of the best ways to improve your credit rating.

Perks and rewards: Many cards offer cashback, loyalty points, or travel insurance as an added bonus for your spending.

Cons

The "free money" trap: The lack of immediate interest can psychologically encourage you to overspend or buy things you wouldn't usually afford. This can lead to a habit of relying on debt rather than savings.

The "revert rate" shock: If you fail to clear your full balance before the 0% period ends, the interest rate will jump to the card's standard APR (often around 24.9% or higher), which can quickly become expensive.

Potential credit score damage: Applying for a card causes a temporary dip in your score. Furthermore, if you max out your card (known as high credit utilisation) or miss a monthly repayment, your credit score will suffer.

Loss of 0% deal: With most cards, if you miss a single minimum payment or are late, the lender has the right to withdraw the 0% offer immediately, meaning you start paying interest straight away.

0% purchase card FAQs

How long will it take to get a card?

It usually takes around 10 days for your card to arrive once you have applied. Here is how long it can take and how to speed up the process.

Does my credit record matter?

Yes, your credit record matters as it helps lenders decide whether to accept you as well as what APR and credit limit they will offer you.

How do I repay my credit card?

The best way to repay your credit card is to set up a Direct Debit to pay off the full balance. This means you will never miss a payment or pay interest. Here are all the ways to repay.

What are minimum payments?

Your provider will set a minimum amount you have to pay back each month. However, it’s best to pay off more than this if you can. If you don’t meet the minimum payment, you will be charged a fee of around £12, and the missed payment will be noted on your credit record.

Can I do a balance transfer with a 0% purchase card?

No, you can't do a balance transfer unless it is to a combined balance transfer and purchases card. If you do this, you can transfer what you owe on a credit card to a new deal with a better interest rate.

About the author

Didn’t find what you were looking for?

Below you can find a list of our most popular credit cards:

Customer Reviews

by 1,077 people

Everything you need to gain credit for…

Everything you need to gain credit for your business

Michael Ver-yard

Very fast and efficient. From start to finish it was easy to follow the application.

Very fast and efficient.

SAL

Great website

Great website, very easy to use and compare options. Clear information and really helpful for making decisions quickly.

customer

We’ve been featured in