- >

- Credit cards>

- Our best money transfer credit cards | Compare deals for June 2026

Compare our best 0% money transfer credit cards

Transfer cash to your bank account with a credit card

Check eligibility and compare 0% money transfer credit cards

What is a money transfer card?

A money transfer card allows you to borrow money from your credit card and transfer it directly into your bank account. Typically, there is a fee for this service, usually around 4% of the amount transferred.

How does it work?

The transfer takes place after you ask your provider to transfer the money into an account of your choosing.

This should not be confused with withdrawing money from your credit card from an ATM, which is known as a "cash advance" and typically results in extra fees and interest charges.

The money transfer facility is useful if you need to pay off an overdraft, or if you need cash to pay for goods and services. An example would be paying a builder or plumber because they don't accept credit card payments.

With a 0% money transfer credit card, not only can you move cash into your bank account, but you can pay off your balance without paying interest for a set period. This could be up to a year or more.

However, to qualify for the longest 0% interest periods, you need to have a good credit score. A cash transfer fee, typically of 3% to 5% would still normally apply.

Why would you get a money transfer card?

Money transfer credit cards are good at doing a very specific set of things.

But if you step outside their specialist areas, they become at best a compromise and quite possibly the entirely wrong product to take out.

So, what are they good for?

The first thing they can help with is clearing an overdraft. With banks now charging as much as 40% interest on overdrafts, moving that cash to a 0% credit card could save you a lot of money.

The second thing they are highly effective at is providing a cheap loan that you can use to pay friends, tradespeople or anyone else you owe money to but who doesn't take credit cards.

But if you're looking to save on existing credit card debt, you'll almost certainly get a better deal with a balance transfer credit card than with a money transfer card.

And if you're looking to spend the money you transfer on anything you can buy directly with a credit card, a 0% purchase card will work out cheaper.

If you're looking to borrow more than £5,000, it's worth looking into a traditional loan as well, then comparing the total costs of each.

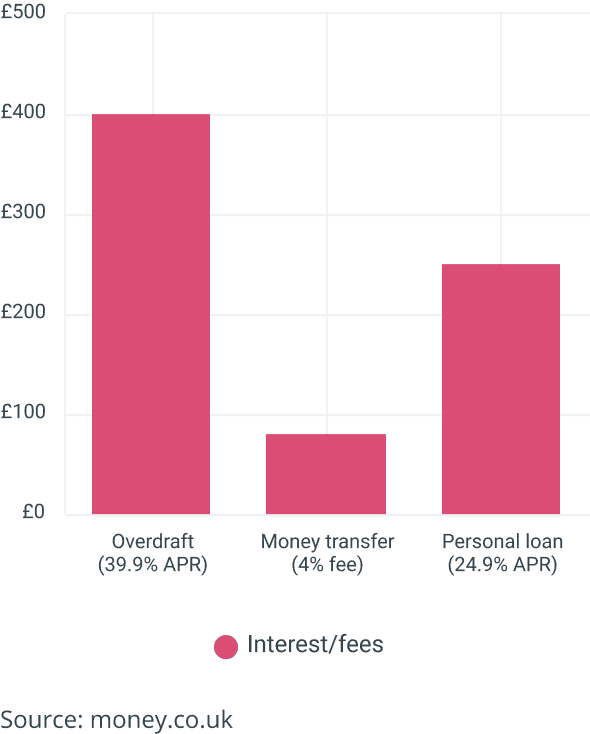

Borrowing £2,000 over 12 months with a loan, money transfer or overdraft

Pros and cons

Pros

Cons

How to choose the best money transfer card

Interest free period

This is the period during which you don’t pay interest on your balance, and begins once you’ve made the transfer. In most cases this should happen within days of receiving the card. The longer the interest free period, the less you’ll have to pay each month to pay off your debt before the 0% period ends.

Money transfer fee

Most money transfer credit cards will charge a fee to transfer the money. This is either a flat fee or a small percentage of the amount you want to transfer - usually around 3% to 5% of the amount you transfer - and is added to the balance on your new card.

Interest rate

This is the rate you’ll be charged to borrow on your credit card after the interest free period ends. It’s often known as the revert rate. If you plan on continuing to use your card after the 0% period ends, it’s important to get a card with the lowest rate you’ll be accepted for, especially if you think you’ll be carrying over a balance on a regular basis.

Check eligibility and compare 0% money transfer credit cards

What if I can't afford to keep up with payments?

If you’re having trouble keeping up with your payments, don’t be afraid to ask for help. There are several independent services you can contact for free advice.

As well as helping you to manage your debts, these services can also ensure you are receiving all the benefits you are entitled to, including tax credits. This could help top up your income and go towards paying off your debts.

StepChange - StepChange is a charity providing advice and help on budget and debt management. It has a helpline that provides free and independent advice.

Citizens Advice - You can find your local Citizens Advice in the phone book or through its website. Citizens Advice can advise you on legal and financial issues.

National Debtline - The National Debtline offers confidential, free advice to people facing debt problems in England, Wales and Scotland.

Jargon buster

Cash withdrawal

Withdrawing funds from an ATM using your credit card attracts a specific fee (unless you have a travel credit card that doesn't impose cash withdrawal fees at ATMs) and daily interest charged from the moment you take the money out. Be aware that providers often apply these same expensive rules to "cash-like" transactions — such as buying foreign currency, stocks, or placing bets — categorising them exactly the same as an ATM withdrawal.

Credit limit

Your credit limit is the amount you can borrow on your credit card at any one time. If you exceed this amount, you can be charged a fee — typically £12 — and it can leave a mark on your credit report. You won’t usually find out your credit limit until the end of an application process, although you can ask your provider to increase — or decrease — your credit limit at any time.

Credit limits are set based on your credit history and your earnings. Once you've reached your credit limit, you need to make a payment to bring down your balance before you can use the card again. Find out more in our guide to credit limits.

Credit score

Your credit score is calculated based on your credit history. Each credit reference agency has its own method of calculating this. Your credit score will go up for things like making payments on time and down for things like being late or defaulting on a loan. Typically, the higher your score, the more likely you are to be offered a lower rate of interest or higher credit limit.

There is no absolute pass or fail mark attached to a credit score, with each lender making its own decision on what it considers acceptable.

Default

This occurs when the relationship between you and the lender has broken down due to unpaid debt. It typically happens after 3-6 months of missed payments. You will receive a warning letter 14 days prior; if you do not pay, the account is defaulted. This blocks you from using the card and significantly damages your credit rating for six years.

Eligibility criteria

The minimum standards you need to satisfy before a provider will consider your application. This typically involves your age, employment status, and salary. You should check these carefully before applying to avoid unnecessary rejections, though meeting them does not automatically guarantee you will get the card.

Hard credit check

If you’ve made an application for credit, such as a credit card, loan or mortgage, lenders will carry out an in-depth check of your credit report, known as a hard credit check.

This is a detailed look into your financial history, especially your borrowing history, so a lender can see your track record of repaying money you've previously borrowed.

A hard check will show any negative marks on your credit report, like overdue payments, missed payments, previous credit applications and even bankruptcies.

Every time a hard check is carried out, it leaves a mark on your credit report, which can hurt your credit score.

Interest-free credit

Interest-free credit cards allow you to either transfer a balance, make purchases or transfer cash to a current account without paying any interest on your balance for a set period. However, you must keep making at least the minimum monthly repayment during this time.

Once the 0% deal is over, you will be charged interest on any remaining debt at your standard APR. With balance transfers and money transfers, you will usually have to pay a transfer fee.

Introductory offer

Credit card introductory offers include bonus reward points, extra cashback, 0% on balance transfers or 0% on purchases.

Introductory offers are used to attract new customers, but once they expire, they revert to the standard offer or rate. When this happens, you should check if you’re still getting the best deal or whether you need to switch to a different credit card.

Soft credit check

A soft credit check is a top-level view of your financial history. It lets lenders assess you for their offers and can show you what you could be eligible for.

Although a soft credit check is recorded, it doesn’t leave a mark on your credit file. This means that while you can see soft checks when you look at your own report, lenders can't. A soft credit check won’t impact your credit score, but you’ll be able to see if anyone has checked your credit history.

In certain industries, some employers will perform a soft credit check if you’ve recently applied for a job with them.

Transfer fee

A fee charged by providers for the service of moving debt. This is added to your account balance automatically when the transfer goes through. Fees of up to 3.5% are normal for balance transfers, but you should expect to pay slightly more — usually about 5% — for money transfers.

FAQs

What is APR?

The annual percentage rate (APR) is the interest rate at which you will borrow money on your credit card. It's typically stated as a yearly interest rate and includes any fees and costs associated with the card. In most cases you can avoid paying interest by paying off your credit card balance in full by the due date of every billing cycle.

Should I just withdraw it as cash from an ATM instead?

No, because withdrawing cash by credit card can be far more expensive. This guide explains the cost.

Does my credit record matter?

Yes, looking at your credit record helps lenders decide whether to accept you as well as what 0% period and credit limit they will offer you.

What credit limit will I get?

Your card provider will decide your credit limit by looking at your finances and credit record after you apply. Here is how credit limits work and how they are decided.

How do I repay my full balance?

The best way to do this is to pay by Direct Debit as you’ll never miss a payment. Here is how to decide how much to pay each month.

Can I transfer money to pay off my credit card instead?

Yes, you can use a balance transfer instead to pay off what you owe on a credit card. You then repay your new card, and many cards offer 0% interest periods.

How much money can I transfer to my account?

The amount of money you can transfer from your money transfer card depends on your credit limit.

How long does it take for the money to reach my account?

The time it takes for the money from your money transfer credit card to reach your bank account will depend on the card provider. Check the information during the application process and any information you receive if approved. It may be transferred instantly, or you may have to wait a few days.

Is this the best option if I want to borrow cash quickly?

A money transfer credit card can be a good way to borrow and access cash quickly. For example if you need to pay a tradesman, friend or family member for something in cash as they cannot accept payment via credit card. It can also be a helpful option in paying off an overdraft, especially if that's something you find you rely on regularly and the fees and interest rates are getting expensive.

But interest-free periods can be shorter than with other credit cards out there, and you'll need a good credit score to be approved. If you're looking for a credit card to make in-store or online purchases then you may find other credit cards are more appropriate.

About the author

Didn’t find what you were looking for?

Below you can find a list of our most popular credit cards:

Customer Reviews

Everything you need to gain credit for…

Very fast and efficient. From start to finish it was easy to follow the application.

Great website

We’ve been featured in