What is a unit trust?

A unit trust puts your money in the hands of an expert fund manager together with other investors. Here is what you need to know about unit trusts before you invest.

Unit trusts are just one option when investing your money. Each unit trust has a fund manager who buys assets such as bonds or shares on the stock market, which are then included in the fund. The fund is split into units that investors buy. Here we look at how unit trusts work, what you can invest in, and how much it will cost.

What is a unit trust?

A unit trust is an open-ended grouped investment product, which is a complicated way of saying that there is no limit to how many people can invest in it or how much money can be invested.

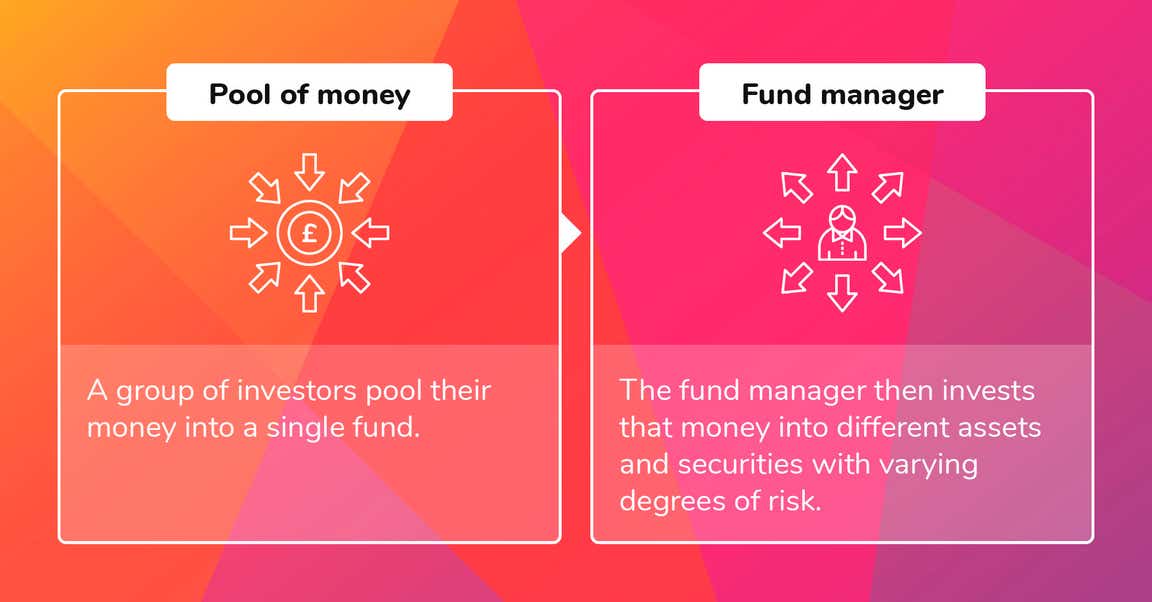

How does a unit trust work?

It works by pooling your money with other investors into a single fund. The fund manager uses the unit trust fund to invest in asset classes through various securities.

What are securities?

Securities are the type of financial instrument held in a unit trust, for example, shares, bonds or gilts.

Not all securities have the same level of risk, so make sure you are happy with the risk involved with your chosen unit trust.

Where do unit trusts invest?

The fund manager will use the unit trust fund to invest in various securities within a specific or selection of asset classes.

Each investment can be further categorised into an investment region, asset classes and industry types. Just some of the different types include:

Asset class: e.g. equities, fixed income and property

Investment region: e.g. global emerging markets, UK, Japan and US

Industry sector: e.g. energy, real estate, utilities and healthcare

By investing in a range of different asset classes, investment regions, and industry sectors, fund managers can diversify where your money is held to try and reduce risk. It avoids putting all of your investment eggs in one basket.

There are many different unit trusts available, and you can find some on the Hargreaves Lansdown website.

How does a unit trust make you money?

You make money by selling your units for more than you bought them.

What is a unit?

When you invest in a unit trust, you buy units in the trust alongside other investors. Each unit has an individual price called the Net Asset Value (NAV). More units are created to meet demand, so there is no limit to how many units are created in a single unit trust.

The NAV reflects the value of the overall unit trust's assets – that is, the investments the fund manager has made with the fund.

Here is how the NAV is calculated:

Unit trust assets minus its liabilities are worth £100,000

50,000 units have already been issued

To find out the NAV, divide the value of the assets by the number of units issued. So, in this example, that’s 100,000 divided by 50,000.

This gives us a NAV of £2

The NAV does not represent the price you will pay for a unit in a unit trust. The price of a unit will be affected by administration costs, such as the initial charge.

When should you sell your units?

Unit trusts aren’t usually considered short term investments. This is because of how buyer and seller prices are calculated using a bid-offer spread.

The way a bid-offer spread is calculated differs between fund managers, but it always represents the difference between how much you buyers will pay per unit and how much sellers want for one.

For example, for a unit trust with a net asset value of £2, the offer price to buy it might be £2.10 while the bid price to sell it is £1.90.

If you buy a unit at the offer price of £2.10, you need to wait until the bid price has risen, otherwise, you stand to lose money.

For this reason alone, a unit trust is not a short-term investment – even in a rising market, it can take time for the unit’s 'sell price' to outperform the original price you paid.

How else can you get a return on your investment?

This depends on whether your unit trust is making money or not and the unit type you invest in, such as:

Income units: Investing in income units means you receive a pay-out up to several times a year*.

Accumulation units: Investing in accumulation units means any income will be reinvested in addition to your existing units*.

If you decide to sell your units, you may be liable for Capital Gains Tax (CGT) if your holdings are not within a self-invested personal pension (SIPP) or an individual savings account (ISA)- visit the GOV.UK website for more information.

* Payments are based on unit trust growth, and do not apply if the trust if underperforming.

What are the fees for investing in a unit trust?

There are a number of charges to look out for when investing in unit trusts, these include:

Brokerage fees: This differs from broker to broker.

Annual management charge (AMC): This can be between 0.5 - 2%, and pays for the management of the unit trust.

Initial charge: This charge can be 3-5% of your deposit. This can often be avoided by investing through a broker. Some funds have exit fees but this is uncommon.

How can you invest in a unit trust?

Broker: You can discuss your unit trust needs with some brokers to find a unit trust that matches the level of risk you are prepared to accept.

Direct through an investment platform: You can apply directly with an investment platform like Hargreaves Lansdown, which will take you through the application process.

Independent financial advisor (IFA): Seek independent advice from an IFA for an unbiased discussion on the type of unit trust you should invest in but make sure you’re aware of the costs.

Before you decide how to invest, it’s important to weigh up all the costs involved and to remember that the value of your investments can go down as well as up. Investing in a unit trust through a broker can save you money on fees compared to investing directly.

About Cathy Hudson

Cathy has been a journalist since 2001, starting her career writing about mortgages and property then becoming editor of a mortgage and home buying magazine. Before going freelance in 2018 she worked at Which? for 12 years, first as a money researcher and writer then as an editor in the money, home, tech and cars teams.

View Cathy Hudson's full biography here or learn more about our editorial policy